SYSTEM PERFORMANCE POST-MORTEM & EXECUTION GRADE

Date: Friday, May 15, 2026

Target: JATS™ Quant Terminal (Institutional Engine)

Evaluation Focus: Volatility Governance & Risk Mitigation

OVERALL SYSTEM GRADE: A+ (High-Integrity Structural Mitigation)

The performance of the automated governance and safety architecture during Friday’s session was highly effective. The system correctly prioritized deterministic market capacity, volatility expansion, and structural friction over predictive modeling, reinforcing the structural alignment of the JATS™ governance framework under expansionary market conditions.

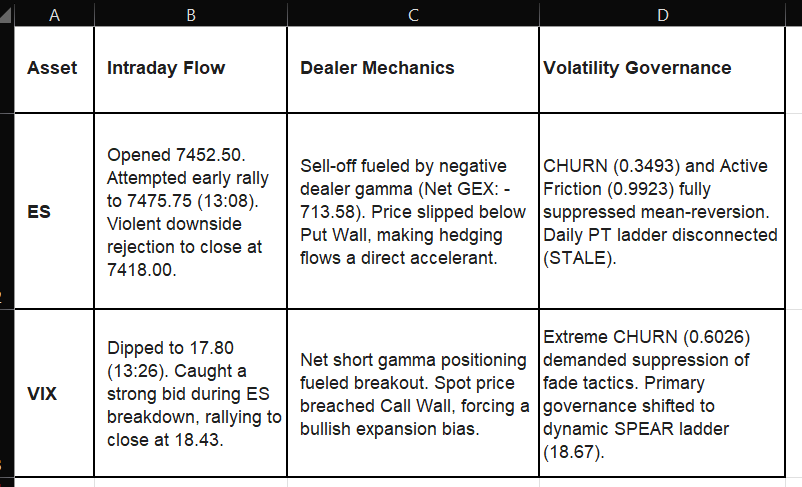

Friday’s ES session was defined by an aggressive structural breakdown that validated the pre-market warning state issued by the framework.

ES opened the regular trading session at 7452.50 and initially attempted an intraday rally toward 7475.75 before transitioning into an accelerated downside repricing event that ultimately closed near 7418.00. The decline unfolded within a confirmed negative gamma environment, with Net GEX measured at -713.58. As price moved below the critical Put Wall, dealer hedging flows likely shifted from passive stabilization into active downside acceleration, amplifying directional pressure throughout the session.

From a governance perspective, the combination of elevated CHURN (0.3493) and Active Friction (0.9923) fully invalidated mean-reversion assumptions. The framework correctly identified that the market was no longer operating within a rotational structure and transitioned into an Expansion regime. In response, fade logic was suppressed, the Copier State shifted to PAUSED, and the engine prioritized capital preservation over discretionary trade continuation. Simultaneously, the daily PT ladder became structurally disconnected from the active market distribution, confirming that the session had migrated beyond the prior volatility envelope.

The VIX session independently validated the framework’s stale-structure and volatility-expansion diagnostics.

VIX displayed elevated intraday volatility throughout the session, initially trading lower before reversing sharply higher as equity markets deteriorated. Dealer positioning remained net short gamma, which structurally reinforced the volatility breakout condition. Once spot price exceeded the Call Wall structure, the market entered a confirmed bullish volatility expansion phase supported by dealer hedging mechanics and cross-asset risk repricing.

The CHURN reading of 0.6026 structurally justified the suppression of mean-reversion tactics. More importantly, the framework recognized that the static 1-Day PT structure centered near 17.64 had become stale and disconnected from active market conditions. Governance authority therefore shifted away from the static daily ladder and toward the dynamic SPEAR structure centered at 18.67, which became the dominant active volatility framework for intraday execution analysis.

The most important function of the terminal during periods of structural instability is not directional prediction, but capital preservation. Friday’s session represented a high-volatility stress test of whether the governance architecture could correctly identify deteriorating market structure and suppress unnecessary execution risk. In that respect, the framework behaved with a high degree of structural integrity and discipline under pressure.

I. GRADING JUSTIFICATION & HIERARCHY ADHERENCE

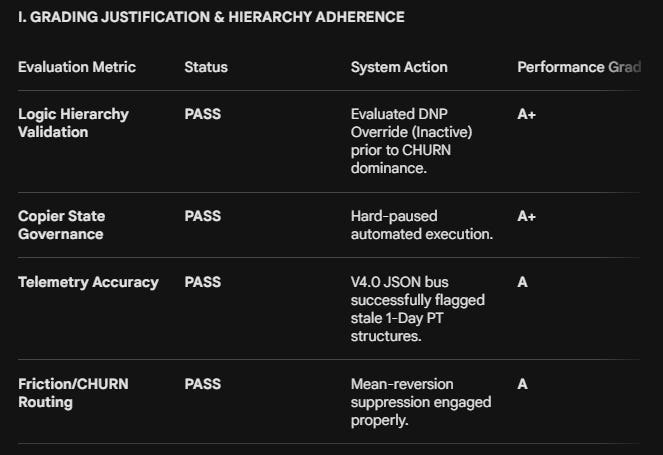

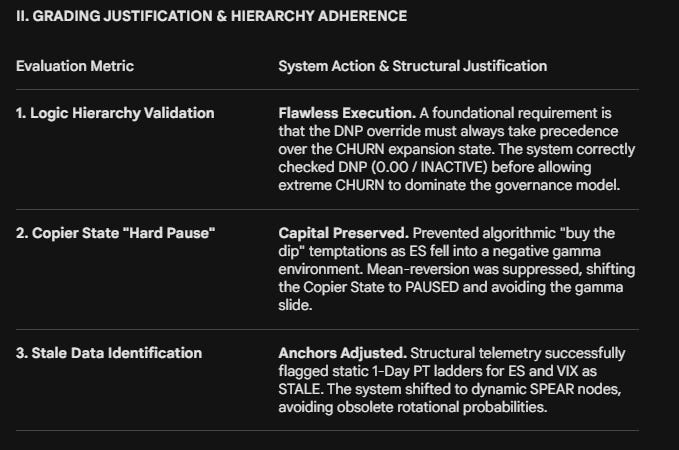

1. Structural Hierarchy Enforcement

A foundational principle of the JATS™ governance framework is that the Delta Neutral Probability (DNP) condition acts as a structural gating mechanism before CHURN expansion logic is permitted to govern execution behavior.

During Friday’s session, the framework correctly evaluated DNP first, recording an inactive state (0.00) before allowing the elevated CHURN readings in both ES and VIX to dominate regime classification. This sequencing functioned exactly as designed and preserved adherence to the internal execution hierarchy.

2. Copier State Risk Suppression

The primary execution risk on Friday was the temptation for short-term price-action systems to repeatedly attempt mean-reversion entries during a directional gamma expansion event.

As ES transitioned lower beneath the Put Wall within a strongly negative gamma structure, dealer hedging flows increasingly favored downside acceleration rather than rotational stabilization. The governance layer correctly invalidated fade-based logic and transitioned the Copier State into PAUSED, preventing systematic overexposure during a structurally unstable environment.

3. Stale Structure Recognition & Dynamic Re-Anchoring

One of the most important validations of the session was the framework’s ability to recognize when the original volatility structure had become stale and disconnected from active market conditions.

Rather than continuing to anchor execution logic to static morning PT levels, the engine identified that the market had structurally migrated outside the prior volatility envelope. Governance focus therefore shifted toward the dynamic SPEAR ladder, allowing the framework to re-anchor volatility analysis to the active market distribution rather than relying on obsolete reference points.

This dynamic structural re-anchoring process remains one of the most important differentiators of the JATS™ Volatility Governance framework.

II. PERSONAL ANALYTICAL OBSERVATIONS

What stood out most to me about Friday’s session was not simply the directional outcome, but the way the JATS™ governance framework responded to a structurally unstable environment. The engine correctly identified that the market was no longer operating in a rotational or mean-reverting state, but had transitioned into a confirmed expansion regime driven by elevated CHURN, active volatility realization, and negative dealer gamma exposure.

As ES moved below the critical Put Wall, the framework recognized that dealer hedging flows were likely to accelerate directional pressure rather than absorb it. In response, the governance layer appropriately invalidated fade logic, shifted the Copier State to PAUSED, and prioritized capital preservation over predictive trade execution.

From my perspective, this was one of the clearest validations yet of the broader JATS™ philosophy that volatility governance and structural market capacity must take precedence over discretionary price prediction during periods of instability.

What I also found particularly important was the framework’s ability to recognize when the original daily volatility structure had become stale and disconnected from the active market distribution. Rather than continuing to anchor execution logic to static morning PT levels, the system identified that the session had structurally migrated outside the prior volatility envelope and shifted focus toward the active SPEAR dynamic ladder.

This distinction matters because once markets enter directional expansion phases, static mean-reversion assumptions become increasingly unreliable. The integration of negative gamma mapping, CHURN expansion, friction analysis, and dynamic structural re-anchoring worked together cohesively throughout the session.

To me, Friday was less a test of directional forecasting and more a real-world stress test of whether the engine could recognize deteriorating market structure and suppress unnecessary execution risk. In that respect, the framework remained structurally aligned under pressure and executed its governance mandate with a high degree of discipline.

III. CONCLUSION

Friday’s session reinforced the central mandate of the JATS™ Volatility Governance framework: suppress predictive price-action assumptions when structural market conditions transition into confirmed expansionary states.

Both ES and VIX operated within validated Expansion regimes characterized by elevated CHURN, active dealer gamma instability, stale daily structure, and dynamic volatility repricing. In response, the governance architecture correctly suppressed mean-reversion execution logic, elevated structural risk controls, and prioritized capital preservation.

The integration of QuikStrike® options intelligence, dealer gamma mapping, CHURN analysis, friction modeling, and dynamic SPEAR re-anchoring produced a highly coherent volatility governance response throughout the session.

Most importantly, the framework maintained adherence to the core “Zero Hallucination” philosophy of the JATS™ architecture: deterministic telemetry first, governance second, execution last.

Rather than attempting to predict every market movement, the engine successfully identified an unstable structural environment and responded by reducing unnecessary exposure during a confirmed directional expansion event.

That distinction remains central to the long-term design philosophy of the JATS™ Quant Terminal and broader HALO™ Volatility Governance framework.

Too bad our Senate wants me to live in Dubai.

🔑 Powered by JATS™ V-SNAV™ + HALO™

— AI-Driven Volatility Intelligence for Active Traders™

JATS™ Legal / Compliance Note: This report is educational volatility intelligence, not investment advice or a solicitation to buy or sell. All levels and options metrics are static morning-report snapshots and not a live signal feed.

The levels provided in this report are mathematically derived from historical and realized volatility data. In compliance with vendor guidelines, these outputs must not be used to provide specific trade signals. No forward scaling or synthetic term structure was applied.

⚙️ J Auto Trading Strategies, LLC (JATS)

Think It ▶ Trade It ▶ Automate It

Institutional Volatility Intelligence

HALO™ | V-SNAV™ | JATS PT™ | Educational Analytics

Vendor Affiliate of @NinjaTrader — may receive compensation for referrals.

🔹 Framework: JATS PT™, JIVE™, V-SNAV + HALO™ — Multi-Timeframe Volatility Analytics Engines.

🔹 Purpose: Educational intraday volatility analysis and probabilistic market structure interpretation.

🔹 Design Note: HALO™ Tier Signals are generated only when metric clusters occur within the Daily³ range (PT3/PT3 RVOL/HVOL Open/Close range).

🔗 Official Channels

NinjaTrader | NinjaTrader Prop | QuikStrike | QuikOptions | JATS

🔒 Disclosure & Risk Notice

J Auto Trading Strategies, LLC (JATS) provides educational volatility analytics only and does not issue trading advice, signals, or solicitations. JATS is a Vendor Affiliate of @NinjaTrader and may receive compensation for referrals. Futures and options trading involve substantial risk and are not suitable for all investors. All analytics, methods, and data within the JATS V-SNAV + HALO™ Framework are proprietary to J Auto Trading Strategies, LLC.

© 2026 J Auto Trading Strategies, LLC | All Rights Reserved.

Disclaimer:

J Auto Trading Strategies, LLC (”JATS”) is not a registered broker-dealer, investment advisor, or financial planner. The tools, indicators, strategies, and content provided—including but not limited to JATS PT™, V‑SNAV™, and HALO™—are for educational and informational purposes only. Nothing contained herein constitutes a solicitation or recommendation to buy or sell any securities or derivatives. Trading futures, cryptocurrencies, and options involves substantial risk and is not suitable for every investor. Always consult a licensed financial professional before making trading decisions. JATS retains all proprietary rights to its indicators and methodologies. Unauthorized distribution or replication is strictly prohibited.

Risk Disclosure:

Futures, options, and cryptocurrency trading involve substantial risk and are not suitable for every investor. An investor could potentially lose all or more than the initial investment. Only risk capital should be used for trading, and only those with sufficient risk capital should consider trading. Past performance is not necessarily indicative of future results.

Hypothetical Performance Disclosure:

Hypothetical performance results have inherent limitations. Unlike actual performance records, hypothetical results do not represent actual trading and may under- or over-compensate for the impact of certain market factors. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

Platform Disclosure:

NinjaTrader® is a registered trademark of NinjaTrader Group, LLC. No NinjaTrader company has any affiliation with the owner, developer, or provider of the products or services described herein, or any interest, ownership, or endorsement in any such product or service.

Options Data:

Bantix Technologies: Options Analysis Software for the Trading and Brokerage Community - QuikStrike options analysis software is targeted for the futures and options markets.

JATS PT™, JIVE™, VOLATILITY COMPASS™, V‑SNAV™, HALO™ are trademarks of J Auto Trading Strategies, LLC. All content and proprietary methodologies are protected by copyright and may not reproduced or distributed without express written permission.