Here is the post-mortem narrative analysis and performance review based on the provided JATS™ telemetry files for May 22, 2026.

I. Executive Post-Mortem Summary

The May 22, 2026, session played out as a textbook example of volatility containment governed by dealer gamma positioning. The AI-driven volatility intelligence successfully identified a transitional regime where rotational mean-reversion was the primary structural mandate. The session effectively demonstrated how liquidity absorption behaves at predetermined 1-Day HVOL (Historical Volatility) boundaries before magnetic mean-reversion takes control.

II. ES (E-mini S&P 500) Narrative Analysis & Grade

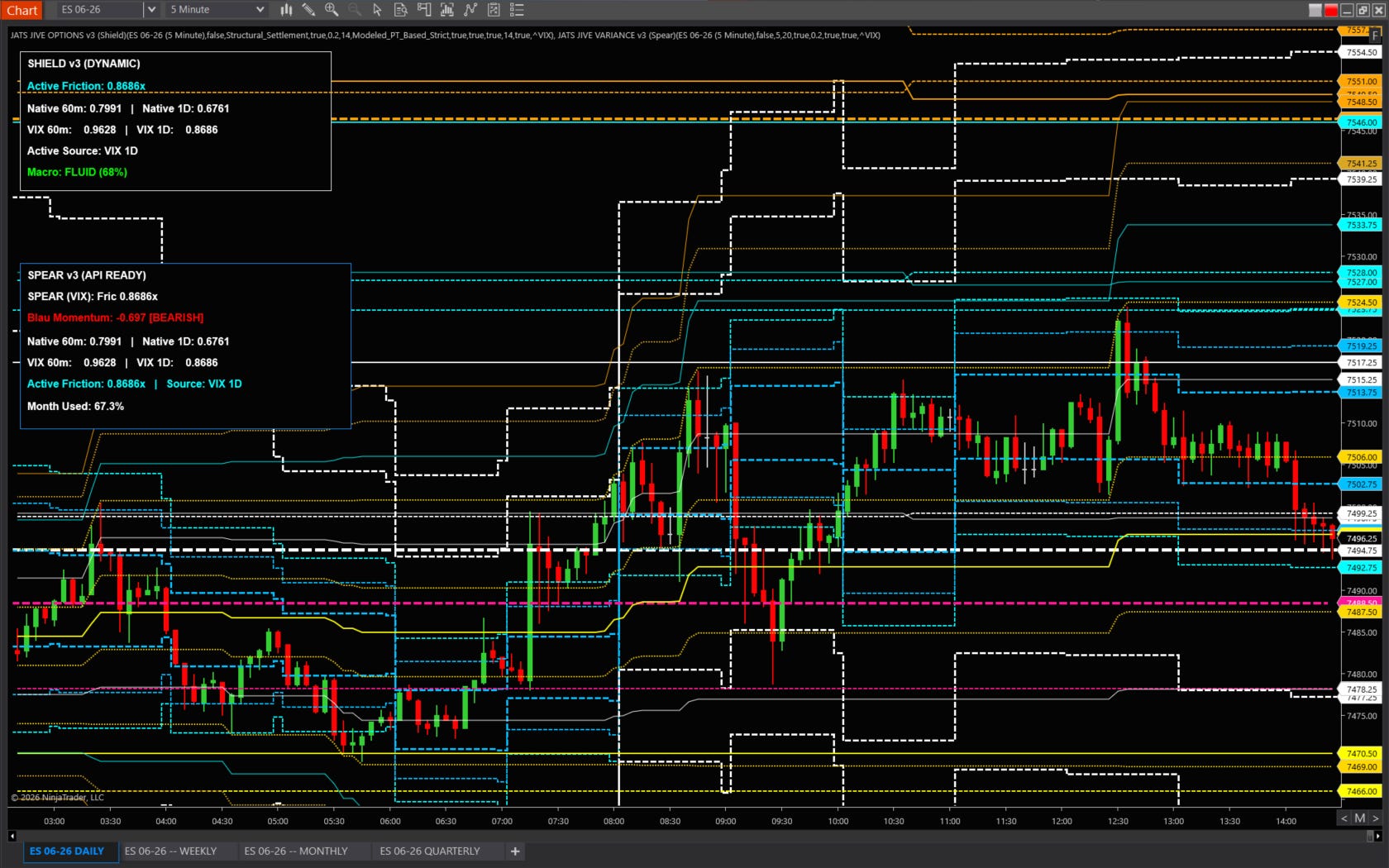

Forecast vs. Execution Reality The primary morning thesis for ES was classified as a “Transitional Regime” with a “Rotational / Mean Reversion” structural bias. The execution map defined the primary trade path as fading tests of the Short Zone at 7494.75 and the Long Zone at 7439.25, targeting the Mean Magnet at 7478.08 and the Gamma Pin at 7475.00.

The intraday price action aligned perfectly with this structural thesis.

The session opened at 7467.0.

The market pushed upward to test the designated 1-Day HVOL PT1A Short Zone (7494.75), piercing it slightly to hit a session High of 7500.50.

At this extreme, the anticipated liquidity absorption and momentum slowdown occurred, triggering the secondary risk condition (breakout risk) to fail as overhead supply capped the market below the 7520 Call Wall.

Following the rejection at the upper standard deviation boundary, price mean-reverted precisely to the dominant equilibrium magnet, printing a LAST price of 7474.75—just 0.25 points away from the 7475.00 Zero Gamma Pin.

Overall ES Grade: A+ The intelligence framework perfectly mapped the intraday boundaries and the closing magnet. Traders following the primary “Fade Valid” playbook at the 7494.75 short zone were heavily rewarded as the market rotated directly to Target 1 (Mean: 7478.08) and Target 2 (Options Magnet: 7475.00).

III. VIX Narrative Analysis & Grade

Forecast vs. Execution Reality A complete analysis of the standalone VIX telemetry is heavily restricted. The dedicated VIX payload suffered from systemic telemetry failure, reporting “DATA MISSING” for critical metrics including CHURN, Friction, DNP, and VUR.

However, cross-asset context derived from the ES reports provides a partial macro picture. The VIX LAST was recorded at 17.02. The ES analytical framework correctly interpreted this reading as indicative of a “neutral” macro volatility state that lacked the extreme fear necessary to force a systemic trend or override the ES-specific options structures. The lack of cross-asset pressure allowed the ES mean-reversion thesis to play out undisturbed.

Overall VIX Grade: INCOMPLETE (N/A) Due to the missing core VIX metrics (CHURN, Friction, VUR), an accurate performance grade cannot be assessed for the VIX-specific forecasting model. However, the interpretation of the VIX’s spot price within the broader ES cross-asset context was highly accurate and supported the winning daily thesis.

IV. Performance Data Tables

| Asset | Metric / Level | Forecasted Boundary / Target | Actual Print | Variance |

|---|---|---|---|---|

| ES | High (Short Zone Test) | 7494.75 | 7500.50 | +5.75 pts (Liquidity Sweep) |

| ES | Low (Containment) | 7439.25 (Long Zone) | 7466.75 | +27.50 pts (Never tested) |

| ES | Close / Last (Magnet) | 7475.00 (Gamma Pin) | 7474.75 | -0.25 pts (Perfect Pin) |

| VIX | Macro State Indicator | Range-bound / Neutral | 17.02 | N/A |

| Asset | Playbook Bias | Execution Path | Market Outcome | Model Grade |

|---|---|---|---|---|

| ES | Rotational / Mean Revert | Fade extensions near 7494.75 | Rejected at 7500.50, reverted to 7475 | A+ |

| VIX | N/A (Data Missing) | N/A | Maintained neutral cross-asset equilibrium | INCOMPLETE |JATS Note> We are working hard on updating the telemetry for the updated Terminal and still have some work to do. But are optimistic that we will be able to complete all bug fixes and get this rolled out in early June.

HAGD and Weekend! See you Tuesday!

🔑 Powered by JATS™ V-SNAV™ + HALO™

— AI-Driven Volatility Intelligence for Active Traders™

JATS™ Legal / Compliance Note: This report is educational volatility intelligence, not investment advice or a solicitation to buy or sell. All levels and options metrics are static morning-report snapshots and not a live signal feed.

The levels provided in this report are mathematically derived from historical and realized volatility data. In compliance with vendor guidelines, these outputs must not be used to provide specific trade signals. No forward scaling or synthetic term structure was applied.

⚙️ J Auto Trading Strategies, LLC (JATS)

Think It ▶ Trade It ▶ Automate It

Institutional Volatility Intelligence

HALO™ | V-SNAV™ | JATS PT™ | Educational Analytics

Vendor Affiliate of @NinjaTrader — may receive compensation for referrals.

🔹 Framework: JATS PT™, JIVE™, V-SNAV + HALO™ — Multi-Timeframe Volatility Analytics Engines.

🔹 Purpose: Educational intraday volatility analysis and probabilistic market structure interpretation.

🔹 Design Note: HALO™ Tier Signals are generated only when metric clusters occur within the Daily³ range (PT3/PT3 RVOL/HVOL Open/Close range).

🔗 Official Channels

NinjaTrader | NinjaTrader Prop | QuikStrike | QuikOptions | JATS

🔒 Disclosure & Risk Notice

J Auto Trading Strategies, LLC (JATS) provides educational volatility analytics only and does not issue trading advice, signals, or solicitations. JATS is a Vendor Affiliate of @NinjaTrader and may receive compensation for referrals. Futures and options trading involve substantial risk and are not suitable for all investors. All analytics, methods, and data within the JATS V-SNAV + HALO™ Framework are proprietary to J Auto Trading Strategies, LLC.

© 2026 J Auto Trading Strategies, LLC | All Rights Reserved.

Disclaimer:

J Auto Trading Strategies, LLC (”JATS”) is not a registered broker-dealer, investment advisor, or financial planner. The tools, indicators, strategies, and content provided—including but not limited to JATS PT™, V‑SNAV™, and HALO™—are for educational and informational purposes only. Nothing contained herein constitutes a solicitation or recommendation to buy or sell any securities or derivatives. Trading futures, cryptocurrencies, and options involves substantial risk and is not suitable for every investor. Always consult a licensed financial professional before making trading decisions. JATS retains all proprietary rights to its indicators and methodologies. Unauthorized distribution or replication is strictly prohibited.

Risk Disclosure:

Futures, options, and cryptocurrency trading involve substantial risk and are not suitable for every investor. An investor could potentially lose all or more than the initial investment. Only risk capital should be used for trading, and only those with sufficient risk capital should consider trading. Past performance is not necessarily indicative of future results.

Hypothetical Performance Disclosure:

Hypothetical performance results have inherent limitations. Unlike actual performance records, hypothetical results do not represent actual trading and may under- or over-compensate for the impact of certain market factors. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

Platform Disclosure:

NinjaTrader® is a registered trademark of NinjaTrader Group, LLC. No NinjaTrader company has any affiliation with the owner, developer, or provider of the products or services described herein, or any interest, ownership, or endorsement in any such product or service.

Options Data:

Bantix Technologies: Options Analysis Software for the Trading and Brokerage Community - QuikStrike options analysis software is targeted for the futures and options markets.

JATS PT™, JIVE™, VOLATILITY COMPASS™, V‑SNAV™, HALO™ are trademarks of J Auto Trading Strategies, LLC. All content and proprietary methodologies are protected by copyright and may not reproduced or distributed without express written permission.